Norbert Sasse

Growthpoint Properties

Group CEO

Estienne de Klerk

Growthpoint Properties

SA CEO

“Growthpoint’s diversified portfolio and income streams, and its embedded sustainability, which are all constantly being improved by skilled leadership and dedicated teams, position it strongly for FY26. The positive momentum across the portfolio is clear, and it is being driven by operational resilience and strategic execution,” says Sasse, who will lead the business for one more financial year before handing over the Group CEO role to current SA CEO Estienne de Klerk on 1 July 2026.

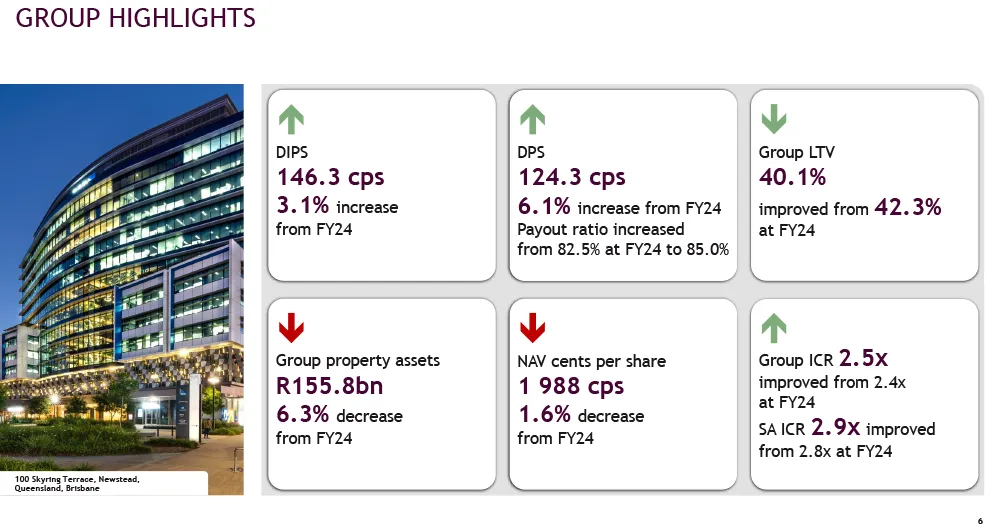

Growthpoint Properties (JSE: GRT) has turned the corner sooner than expected. For the year ended June 2025, the group delivered distributable income per share (DIPS) of 146.3c, up 3.1%, and declared a dividend per share (DPS) of 124.3c, a 6.1% increase. Both numbers beat the top end of guidance.

Growthpoint’s return to growth comes a full year earlier than initially expected.

Growthpoint entered the 2025 financial year (FY25) forecasting an earnings contraction of -2.0% to -5.0%. However, stronger-than-expected performance from its South African portfolio, lower finance costs, and another stellar year from the V&A Waterfront marked a clear turnaround. Better half-year results prompted Growthpoint to upgrade its guidance to positive growth of 1.0% to 3.0%, with a further revision in June 2025 narrowing the range to the upper end of 2.0% to 3.0%.

Norbert Sasse, Group CEO, summed it up: “This strong set of results shows that Growthpoint has done well to exceed expectations and deliver solid earnings growth while executing our strategic priorities. The progress made in further strengthening our SA portfolio is evident in its improved performance. The V&A Waterfront once again delivered stand-out results. Streamlining our international investments has simplified our capital structure and equity story, and disciplined treasury management kept finance costs below expectations.”

A reset on payouts

One of the key changes this year was Growthpoint’s decision to increase its payout ratio. The group paid out 87.5% of distributable earnings in the second half, averaging 85% for the entire year. This boosted dividends ahead of earnings growth.

For FY26, the higher ratio will apply to both halves, which means that with forecasted 3–5% growth in DIPS, shareholders can expect 6–8% growth in DPS.

Sasse clarified that the move back to higher payouts is sustainable, but not unlimited. “We won’t return to 100%. To maintain a resilient business, we need to retain enough to cover maintenance Capex, which typically runs at about R500m–R600m annually. That’s the principle behind our 87.5% policy.”

Balance sheet in better shape

Total assets at year-end stood at R155.8 billion, down from R166.2 billion, mainly due to international disposals. The loan-to-value ratio eased to 40.1% from 42.3%, and the interest cover ratio improved to 2.5 times.

Finance costs decreased, aided by lower borrowings and a reduced cost of debt. In South Africa, the average rate was 8.9% (FY24: 9.6%), while the group average including forex instruments was 6.9% (FY24: 7.2%). Liquidity remains robust, with R900 million in cash and R4.7 billion in undrawn facilities.

“LTV ratios have stabilised. Growthpoint remains committed to resilience and liquidity for the long term,” Sasse stated.

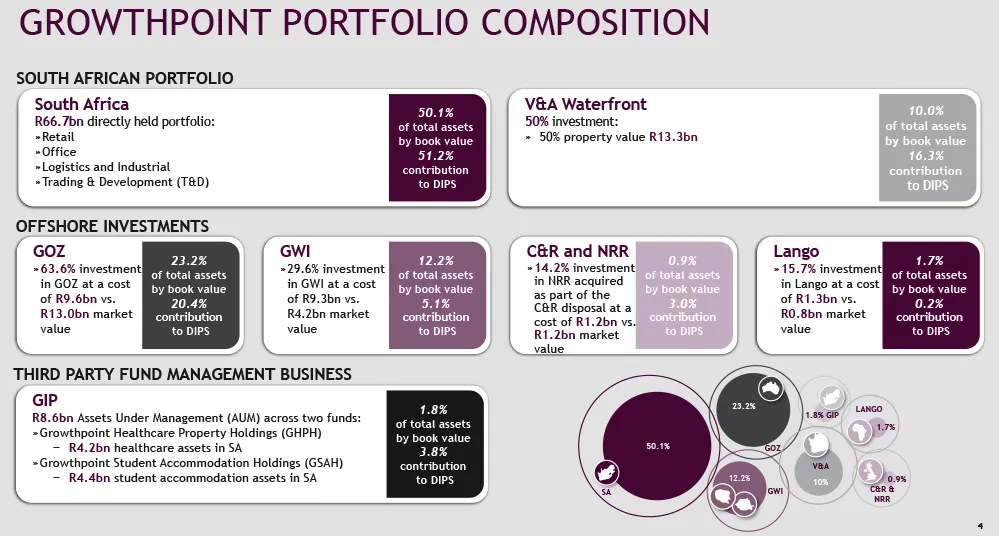

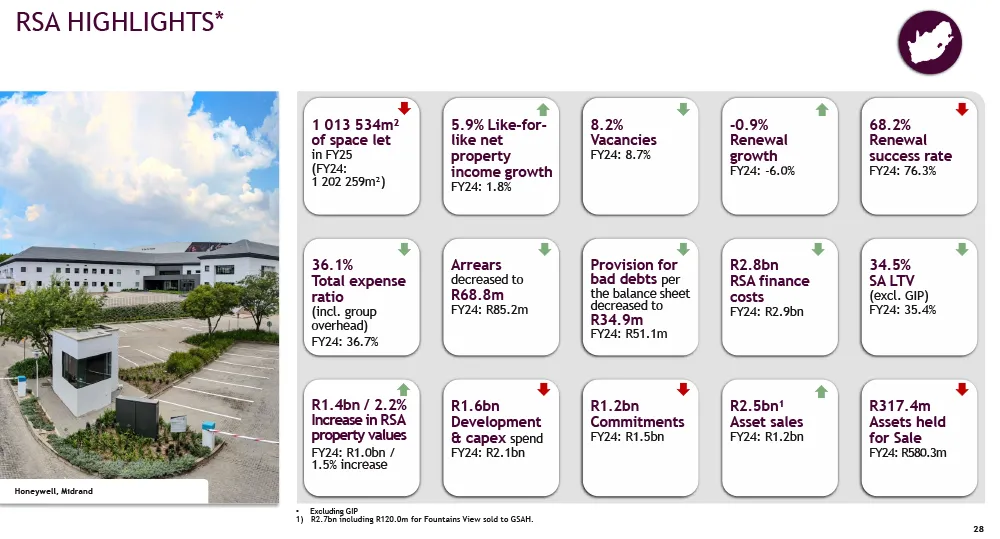

South Africa: momentum returns

The South African portfolio, valued at R66.7bn and comprising just over half of the group assets, was the main driver of growth. Like-for-like net property income increased by 5.9%, vacancies decreased slightly, and arrears were kept under control.

V&A Waterfront: the jewel in the crown

The standout was once again the V&A Waterfront, which the Public Investment Corporation co-owns.

Estienne de Klerk, SA CEO, was optimistic: “The V&A is in a different league. Net property income grew by 10.4%, vacancies are virtually nonexistent at 0.3%, and trading densities are more than double those of other super-regionals. It’s not only retail — hotels, cruise, residential, and offices all contribute.”

Tourism in Cape Town increased by 6%, boosting the V&A’s draw of 24 million visitors during the year. Cruise activity hit record highs with 83 ships and 170,000 passengers, and retail sales rose 5.8% to surpass the R10 billion mark.

The property also shows the benefits of diversifying beyond pure rental income: operating businesses, such as hotels, now account for 16% of NPI. The Radisson Red, Portswood, and Commodore hotels, operated under leases, all performed strongly. The Table Bay Hotel is reopening in phases from December after refurbishment, while a new luxury five-star hotel with branded residences is set to launch in 2026.

On the residential front, the Five Dock Road apartments have been a success. Of the 98 units, 92 are already sold, with prices exceeding R100,000 per square metre. “That will crystallise a significant profit next year,” de Klerk added.

Offices: a long-awaited recovery

After years of downturn, Growthpoint’s office portfolio showed a clear turnaround.

Like-for-like NPI shifted from a decline of 1.0% to growth of 6.8%.

Vacancies decreased to 14.6%.

Renewal growth improved from a fall of 14.8% to 3.2%, with over half of leases renewed at equal or higher rentals.

Valuations increased by 1.9%, marking the second year of positive revaluations in a row.

“We achieved the first positive office valuation in eight years — about R500 million on a R27 billion portfolio,” said de Klerk. “Vacancies are easing, reversions are improving, and like-for-like income is up nearly 7%. That’s a real shift.”

Developments are also helping to reposition the portfolio.

The Longkloof precinct in Cape Town, including the Canopy by Hilton, is complete. The 36 Hans Strydom redevelopment for asset manager Ninety One is on track to finish this year, and a striking new pedestrian bridge is being built across Sandton Drive.

Industrial & logistics: the quiet engine Industrial has been Growthpoint’s most reliable performer.

Like-for-like NPI increased by 5.5%.

Portfolio valuations grew by 3.1%.

Nearly 60% of new or renewed leases were signed at equal to or higher rental rates.

At the Arterial Industrial Estate in Blackheath, Cape Town, the second phase is now fully let, while new units at Centralpoint have added to a logistics-heavy pipeline.

“Industrial remains the best-performing sector,” said de Klerk. “Positive reversions are broadening, and demand in the Western Cape is supporting more speculative development.”

Retail remains steady, with trading and development selective

The retail portfolio maintained stability, with like-for-like NPI up 5.3% and vacancies low at 4.4%. Trading densities increased 4.8%, ahead of the Clur benchmark, with community centres and Western Cape malls leading.

Growthpoint’s Trading & Development division produced R51.6 million in trading profit and is preparing for a new cycle of third-party projects, including the Olympus Sandton residential towers, in partnership with Tricolt.

International: simplification proves beneficial

Growthpoint has been reshaping its offshore exposure.

By year-end, 38% of assets and 28.7% of DIPS were offshore.

Australia (GOZ) contributed 20.4% of DIPS. Distributions dipped to AUD18.2cps from AUD19.3cps, but a special payout offset tax withholdings.

Occupancy remains high at 94%, with a WALE of 5.6 years.

The funds management arm gained momentum with a new AUD198 million logistics partnership and a Canberra office trust. Central & Eastern Europe (Globalworth) contributed 5.1% of DIPS.

While distributions fell 33% to EUR14.0cps due to higher finance costs and Polish tax changes, the balance sheet was strengthened, and cash dividends were resumed.

Lango (Pan-Africa) contributed 0.2% of DIPS, boosted by a USD 200 million acquisition from Hyprop and Attacq. The UK investment was fully exited after year-end.

Sustainability: expanding influence

Growthpoint has invested R1 billion in solar energy, with 80 plants and a capacity of 61.2 MWp. In October, it will launch e-co₂, providing tenants with certified zero-carbon power at cost-escallation rates, supported by a 195GWh PPA with Etana Energy.

It is also aiming for 89.4ML in water savings over three years, with 43% of waste diverted from landfills.

Looking forward

Growthpoint expects the property cycle to enter a growth phase, supported by lower interest rates and stronger fundamentals.

The group targets R3.5 billion in non-core disposals in FY26, while increasing focus on logistics, high-demand offices, and precinct development.

The V&A Waterfront, already a major contributor, is expected to deliver double-digit growth next year as refurbished hotels reopen and residential sales are transferred.

Sasse concludes: “Growthpoint’s diversified portfolio and income streams, and its embedded sustainability, position it strongly for FY26. The positive momentum across the portfolio is evident and driven by operational resilience and strategic execution.”

De Klerk, positive: “The V&A continues to evolve as a globally competitive precinct; offices are finally turning the corner; and industrial remains our quiet engine. We’re investing where demand is strongest, and the portfolio is well positioned for durable growth.”