Norbert Sasse

Growthpoint Properties

Group CEO

Estienne de Klerk

Growthpoint Properties

SA CEO

Growthpoint Properties remains confident in meeting its full-year guidance, despite an uneven first-half performance due to timing differences at the V&A Waterfront and ongoing pressure in parts of its offshore portfolio.

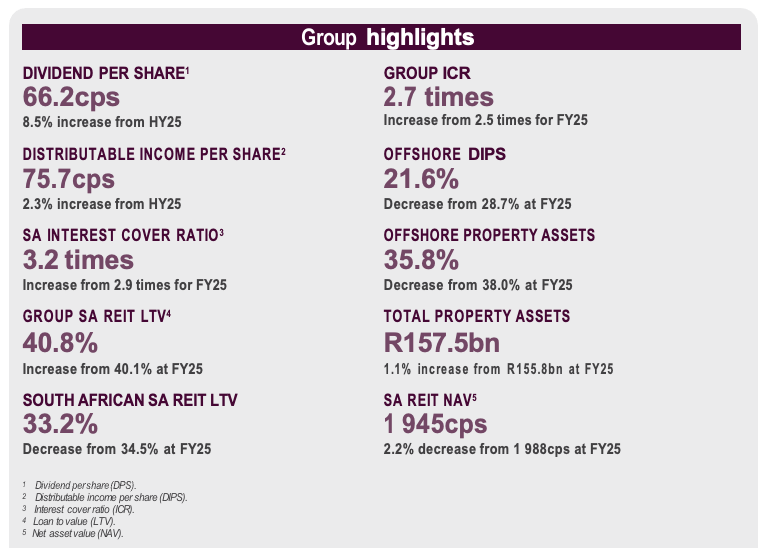

Reporting for the six months to December 2025, the group achieved a 2.3% increase in distributable income per share, while the dividend per share grew by 8.5%, supported by both earnings growth and the higher payout ratio implemented at the end of the previous financial year.

Presenting the results, Norbert Sasse, Group CEO of Growthpoint Properties, stated that the first half was always expected to be uneven.

We projected 3% to 5% growth for the full year and indicated that performance might be somewhat uneven between the first and second halves, primarily due to the V&A Waterfront contribution,” he said.

Although first-half growth was below the full-year range, Sasse said the group remains confident in its outlook.

“We are still quite confident in our full-year guidance range of 3% to 5%,” he said.

Dividend growth and balance sheet discipline

For investors, the most notable headline was the dividend increase. Sasse said the 8.5% rise reflected both growth in distributable income and the higher payout ratio, which moved from 82.5% to 87.5%.

Meanwhile, the group continued to bolster its balance sheet. The loan-to-value ratio remains well managed, with South Africa’s LTV now in the low 33% range. Growthpoint also reduced total debt from just over R39 billion to R36.7 billion, mainly through asset disposals and using the proceeds to repay debt.

Sasse observed that post-period transactions, including the Discovery disposal, will further facilitate deleveraging.

He stated, “We will have almost R2 billion of cash that, in the short term, will be used to further reduce debt.”

The lower debt burden, along with a reduction in the average cost of debt, significantly improved the financing position. Growthpoint’s rand-denominated average cost of debt decreased to 8.5%, from approximately 9.2% in the prior period.

That resulted in a benefit of over R200 million on the interest line compared to the previous period.

South Africa leads the results

The key highlight of the interim result was the robustness of the South African portfolio. According to Sasse, total distributable income in rand increased by about R52 million, with the main positive contributions originating from South Africa and reduced interest costs.

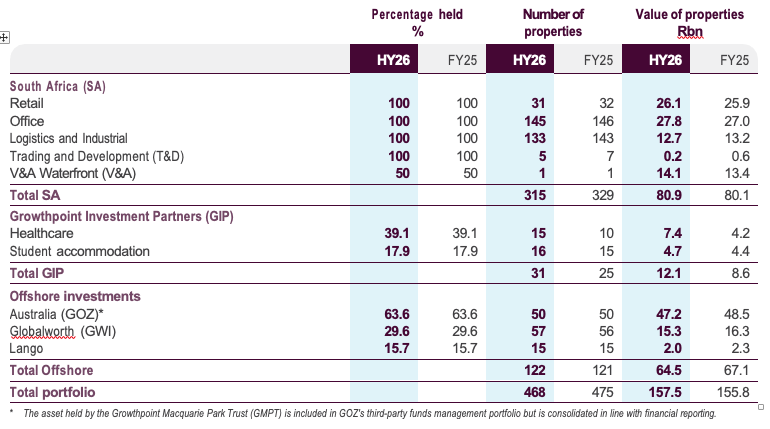

The local portfolio achieved 6% like-for-like net property income growth, with all three core sectors – retail, office, and logistics – contributing positively.

“South Africa is carrying the ship at the moment,” Sasse said, contrasting the current period with the recent past when offshore operations had provided greater support.

He highlighted a 7.5% vacancy rate across the South African portfolio, close to pre-COVID levels, while noting that the only significant ongoing pressure remains in inland office spaces, where rental reversions are still negative on renewal.

Even there, however, operational performance improved. The office portfolio achieved a 5.8% like-for-like net property income growth, supported by cost control and rising occupancy.

Portfolio quality improving

Estienne de Klerk, South Africa’s CEO of Growthpoint Properties, stated that the South African business continues to benefit from a deliberate strategy to enhance portfolio quality whilst selectively reinvesting in stronger assets and nodes.

What we have observed is that, as we have enhanced the quality of the portfolio, alongside improvements in market conditions, it has provided a significantly better contribution to the company,” he said.

Vacancies dropped by one percentage point over the period, with both retail and office sectors improving. Renewal growth remained negative overall, but De Klerk stated this was mainly due to a few significant office renewals that had already been negotiated and flagged at the end of the year.

He added that Growthpoint’s South African balance sheet remains conservatively geared, as reflected in an LTV ratio of 33.2% and a notably stronger interest cover ratio.

The group spent approximately R500 million on developments during the six months and reported remaining development commitments of about R3.5 billion, excluding the V&A Waterfront.

Logistics strategy gains traction

In logistics, Growthpoint’s long-term repositioning strategy continues to evolve. De Klerk said the portfolio has been shifted away from older industrial assets towards higher-quality logistics stock, with the number of industrial properties reduced from more than 220 at its peak to 133 today.

The portfolio is currently valued at approximately R12.7 billion, with vacancies at a low 3.3%.

Although rental growth on renewals remains steady in some areas, De Klerk said the market continues to offer solid fundamentals.

“South Africa is importing more goods and producing less, so logistics is a significant area of growth,” he said. “The dynamics in omnichannel retail have also contributed.”

The logistics portfolio grew by 5.6% like-for-like, while valuation rose slightly.

Retail remains resilient

Growthpoint’s retail portfolio, now comprising 51 assets valued at approximately R26 billion, continued to perform reliably, supported by improved lettings, positive reversions at some centres, and ongoing capital investment in flagship assets.

Vacancies declined to 3.2%, and the portfolio experienced a 6.3% like-for-like growth.

De Klerk said part of the current improvement reflects a catch-up effect after Covid-era lease renewals were concluded on weakened terms.

We are still catching up on the good trading many retailers have experienced in our shopping centres, as they are coming off relatively low rental bases,” he said.

Growth in trading density slowed compared with the prior period, but it still reached 2.3%, broadly in line with recent reports from listed retailers. Regional performance continues to favour the coast, with the Western Cape in particular outperforming Gauteng.

Office recovery continues, but Gauteng lags

The office portfolio displayed further signs of stabilisation, with vacancies decreasing and several key assets experiencing higher occupancy.

De Klerk stated that Durban remains effectively full, Cape Town has very limited vacant space, and Gauteng – though still the most challenged – has started to improve.

“It has been somewhat disappointing in terms of velocity,” he said. “I would have expected the economy to have grown a bit faster by now.”

He stated that the weakness in Gauteng’s office market reflects the broader underperformance of Johannesburg and Pretoria as metropolitan economies, while hybrid working has also altered the nature of demand.

He also argued that the return-to-office trend is gaining momentum.

“I have spoken to every single one of the big four banks, and they are all bringing their staff back,” he said. “Most companies have now moved from three days to four days at a minimum.”

That does not mean office demand remains the same, however. Corporations are increasingly seeking higher-quality, better-equipped spaces that attract employees back into the workplace.

Discovery disposal supports risk management

One of the key capital events during the period was the disposal of Discovery Phase 1 and the acquisition of the minority interest in Phase 2.

De Klerk said that the sale of the first building made strategic sense, despite the asset’s quality and covenants.

“It is a bit of risk mitigation for the future,” he said. “If, in seven years, when the lease is up for renewal, the tenant decides they do not want the entire building, it is a complicated building to subdivide.”

The released capital will initially be utilised to further reduce debt.

Waterfront second-half boost expected

At the V&A Waterfront, interim earnings were affected by the temporary closure of the InterContinental Table Bay hotel and the luxury retail mall during redevelopment. These closures resulted in the Waterfront’s contribution appearing modest in the first half.

However, underlying trading remained robust. Excluding the temporary closures, the Waterfront achieved 8.7% like-for-like property income growth, driven by strong tourism activity and increasing footfall.

Sasse said the second half is expected to be significantly stronger as the reopened hotel increases its operations, luxury retail resumes trading, and profits from the transfer of 5 Dock Road residential units are recognised.

All of those factors indicate we are expecting double-digit growth in the distributable income contribution from the Waterfront for the entire financial year,” he said. De Klerk stated that the average selling prices at 5 Dock Road surpassed expectations by a considerable margin.

Most of the units sold at over R100,000 per square metre, with some nearing R140,000 per square metre, he said.

He added that demand mainly originated from local buyers rather than offshore purchasers, highlighting the resilience of the domestic luxury residential market.

Long-term Waterfront pipeline secured

Growthpoint and its V&A Waterfront partner, the PIC, also gained approval for rights to 440,000 square metres of bulk space, offering insight into development potential over the next twenty years.

The long-term development pipeline is estimated at approximately R20 billion. However, management emphasised that not all of that capital would remain permanently tied up on the balance sheet, as some components will be developed for sale or structured to recycle capital.

Projects currently underway at the Waterfront are valued at between R3 billion and R4 billion, shared by Growthpoint and the PIC.

These include the redevelopment of the InterContinental, the Marriott Edition, and a build-to-rent residential component designed to increase access to the precinct.

De Klerk said the shoreline protection and sea-edge development proposals remain strategically important, not only for asset protection but also for public amenity and tourism value.

GIP grows to R12 billion

Growthpoint Investment Partners continued to expand, with assets under management rising to R12 billion across its healthcare and student accommodation platforms.

The biggest increase came from the acquisition of the Auria later-living business, which contributed about R3 billion in assets to the healthcare fund.

“The game is funds under management, and we have grown that to R12 billion,” De Klerk said.

Management fees from the platform increased by approximately 16% compared to the previous period, and the group anticipates further gains in the second half.

Offshore remains mixed

International operations remain the weakest area of the portfolio. Capital & Regional has now been fully divested, while Globalworth and Growthpoint Australia continue to face market-specific headwinds.

Sasse stated that Growthpoint Australia remains central to the group’s diversification strategy, despite Australia being out of step with other markets on interest rates and still facing inflation pressures.

Operational metrics remain robust, but earnings continue to be impacted by a higher-cost debt environment and slower-than-expected growth in funds under management.

At Globalworth, the decline in contribution was primarily due to a Polish tax charge rather than weak operational fundamentals. Occupancy and letting remain relatively steady, while management has taken steps to strengthen the balance sheet, including bond buy-backs funded from surplus cash.

Outlook unchanged

Despite global uncertainty, geopolitical volatility, and the risk that lower interest rates may take longer to materialise than previously expected, Growthpoint states that the underlying business remains on course. Sasse said that the strength of the South African platform, expected second-half growth from the Waterfront, stable performance from GIP, and broadly in-line offshore results give management confidence in its full-year outlook. “We remain confident that we will meet the forecast of 3% to 5% growth in distributable income per share,” Sasse said. With the higher payout ratio in place, it is expected to lead to 6% to 8% growth in dividend per share for the full year.